Latest News

Biden Looks To Prevent Future President From Ending Ukraine War With 10-Year Agreement

Biden Looks To Prevent Future President From Ending Ukraine War With 10-Year Agreement

Soon on the heels of President Biden last week signing into law a $61 billion aid package for Ukraine’s defense, President Volodymyr Zelensky on Sunday indicated that he’s working with Washington on a bilateral security agreement which would last ten years.

“We are already working on a specific text,” Zelensky said in his nightly video address. “Our goal is to make this agreement the strongest of all.”

Ukrainian Presidential Press Office via AP

{kind=link}

“We are discussing the specific foundations of our security and cooperation. We are also working on fixing specific levels of support for this year and the next 10 years.”

He indicated it will likely include agreements on long-term support centering on military hardware and joint arms production, as well as continuing reconstruction aid. “The agreement should be truly exemplary and reflect the strength of American leadership,” Zelensky added.

But ultimately a key purpose in locking such a long-term deal in would be to keep it immune from potential interference by a future Trump administration.

Below is what The Wall Street Journal spelled out last year:

The goal is to make sure Ukraine will be strong enough in the future to deter Russia from attacking it again. More immediately, Ukraine’s Western allies hope to discourage the Kremlin from thinking it can wait out the Biden administration for a potentially more sympathetic successor in the White House.

Western officials are looking for ways to lock in pledges of support and limit future governments’ abilities to backtrack, amid fears in European capitals that Donald Trump, if he recaptures the White House, would seek to scale back aid. Trump has a wide lead in early polling in the Republican presidential primary field, but soundly lost the 2020 election to President Biden and has been indicted in four criminal cases in state and federal courts.

We and others have previously underscored that NATO and G7 countries are desperately trying to “Trump-proof” future aid to Ukraine and the effort to counter Russia.

As for its first new weapons package in the wake of the $61 billion being authorized, the Biden administration has announced new arms packages totaling $7 billion. The US has vowed to rush the weapons to Kiev, given that by all indicators its forces are not doing well on the frontlines.

“We are still waiting for the supplies promised to Ukraine – we expect exactly the volume and content of supplies that can change the situation on the battlefield in the interests of Ukraine,” Zelensky had said over the weekend. “And it is important that every agreement we have reached is implemented – everything that will yield practical results on the battlefield and boost the morale of everyone on the frontline. In a conversation with Mr. Jeffries, I emphasized the need for Patriot systems, they are needed as soon as possible.”

Zelensky announces that Ukraine is working on a security agreement with the U.S. that will fix levels of support for the next 10 years. The $61 billion was just the beginning. The next two U.S. presidents won’t be able to switch it off. pic.twitter.com/q1RWCxf93m

— David Sacks (@DavidSacks) April 28, 2024

But all of this means the war will be prolonged, and this puts negotiations much further away on the horizon, despite what are now daily acknowledgements of Ukraine forces being beaten back. Currently the governments of Greece and Spain are being pressured by EU and NATO leadership to hand over what few Patriot systems they possess to Kiev. The rationale is that they don’t need them as urgently as Ukraine does.

Tyler Durden

Mon, 04/29/2024 – 10:00

Intervention Or Not, Yen Bears Will Stay Confident

Intervention Or Not, Yen Bears Will Stay Confident

By Vassilis Karamanis, Bloomberg Markets Live reporter and FX strategist

Unless Japanese authorities show their hand with conviction when it comes to intervening in the spot market, the yen is bound to stay under pressure over the medium-term.

The currency’s sharp rally this morning certainly looks like an intervention — it’s not often that we get a 500-pip move seemingly out of nowhere. But thin liquidity due to a public holiday in Japan that forced algorithmic trading to take over as trailing stops were triggered could be what’s driven the market. The fact that traders aren’t sure this is an official hand supporting the yen is telling. Masato Kanda, the nation’s top currency official, said no comment when asked about the moves.

{kind=link}

The market has been testing Japanese authorities’ patience — or determination — when it comes to yen weakness for some time now. And it will keep on doing so for as long as intervention threats are seen as a clumsily-played bluff.

The yen kept breaching through one big level after the other on Friday against the dollar and everyone’s question was whether we would finally have official yen buying before a long weekend in Japan. The answer was an emphatic no.

Did price action Friday actually give Japanese authorities the green light to intervene in the spot market?

The yen fell by the most since October on an intraday basis, for a two standard-deviation move; one-week realized volatility touched a one-month high

It was down 3.5% on a ten-day basis; Kanda said that a 4% move over two weeks doesn’t reflect fundamentals and is unusual

Over one month, the dollar was up by around seven big figures against the Japanese currency; Kanda has said that a 10-yen move over such a time period is considered rapid.

So in nominal terms, we could argue it was justified that no intervention took place, given a simple rates-check during a Japan holiday could actually do the trick. But in real terms, no one would blame Japanese authorities if they went beyond their official guidelines to step in the spot market. It’s not just about the 350-pip day range that took place. It’s the starting point that also matters. Fresh 34-year lows were hit Thursday.

Traders could see lack of official yen buying as an attempt to find excuses in order to stay pat. After all, a weaker currency in theory accelerates inflationary dynamics that will eventually support the Bank of Japan as to signal a more-aggressive-than priced in tightening bias — which could really be a game changing moment for the currency, especially if at the same time the Federal Reserve will indeed be close to easing its own policy.

And as long as credibility comes to the question, the more confident traders will be to re-add dollar longs in case the Ministry of Finance does decide to intervene. There was some speculation during the weekend that Japan is waiting for the Fed meeting and the release of the next US jobs report due this week before deciding to press the button. To me, it doesn’t matter so much if this is credible thinking, but the mere fact traders are discussing it shows the ball is moving away from officials’ court.

It’s not easy going against a central bank. In poker terms, policymakers always start the game with a pair of aces. But the flop did no favors to them and their raise on the turn looks miscalculated. Maybe the upcoming river will see traders winning this hand despite Monday’s retreat for the dollar that at the time of writing has no official confirmation it was down to spot intervention.

Tyler Durden

Mon, 04/29/2024 – 09:45

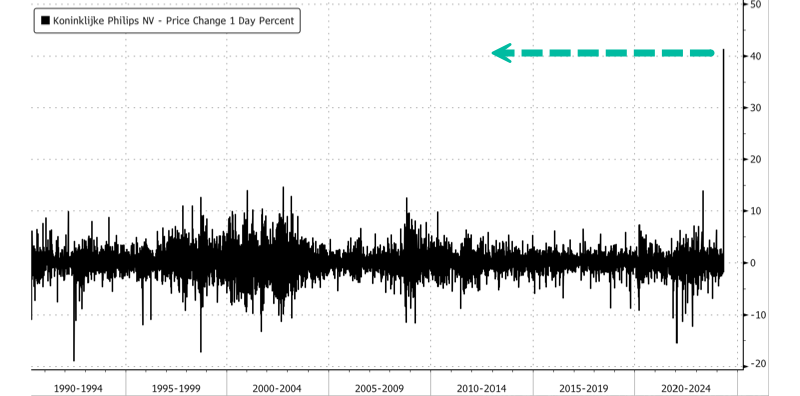

“Much Milder Than Feared”: Philips Shares Soar 43% After US Sleep Apnea Settlement

“Much Milder Than Feared”: Philips Shares Soar 43% After US Sleep Apnea Settlement

Shares of Royal Philips on Euronext Amersterdam surged as much as 43% Monday, the most on record after a lower-than-expected settlement in the US linked to faulty Respironics ventilators for sleep apnea.

The Dutch medical equipment manufacturer recalled the therapy devices due to concerns that the noise-canceling foam inside them was disintegrating, which patients inhaled.

Some Wall Street analysts predicted the company would have to spend as much as $4.5 billion to $10 billion to cover the medical monitoring class-action lawsuit and individual personal injury claims in the US. However, the company only had to set aside $1.1 billion.

Barclays analysts wrote in a note that this earlier-than-expected settlement “removes an overhang many have worried would linger for years.”

Faulty sleep therapy devices have weighed on Philips’s shares since April 2021, tumbling as much as 76% from 48 euros a share to $11.6 in October 2022. Despite today’s 43% surge, shares are still down 40% from the highs recorded in 2021.

{kind=link}

Today’s 43% jump is the largest daily percentage gain ever – beating out the 14.6% gain in 2002.

{kind=link}

The vicious upswing will likely squeeze bears. Data from S&P Global Market Intelligence shows shares out on loan, or an indication of short interest, represented about 4.9% of the company’s float as of Thursday.

Here’s how Wall Street responded to the news (list courtesy of Bloomberg):

Barclays (overweight)

The $1.1b settlement compares with buyside expectations of $2b-$4b, with “worst case fears” of $10b, analyst Hassan Al- Wakeel writes in a note

The earlier-than-expected settlement also “removes an overhang many have worried would linger for years”

Bernstein (market perform)

The settlement amount is less than expected, while the timing is “sooner than thought,” analyst Lisa Bedell Clive writes in a note

Bernstein had been working on the assumption that there was a 35% chance of a €3.8b personal injury settlement, and a 35% chance of a €766m medical monitoring lawsuit

The settlement “removes another overhang on the stock”

Jefferies (underperform)

The unexpected $1.1 billion settlement is “much milder than feared,” marking the “end of litigation uncertainty,” analyst Julien Dormois writes in a note

The 1Q results beat expectations, though order growth fell again

Morgan Stanley (equal weight)

The settlement figure is below expectations and should be well received, analyst Robert Davies writes in a note

There’s scope for FY earnings estimates to be increased by low-single-digits

Morgan Stanley sees questions being raised about the “softness” around the diagnostics & treatment performance, as well as the timeline around a resolution on the consent decree

Philips CEO Roy Jakobs joined Bloomberg TV after the settlement news. He said, “The settlement covers all the claims in the US, even the ones that would come in still over the next six months.”

Tyler Durden

Mon, 04/29/2024 – 09:25

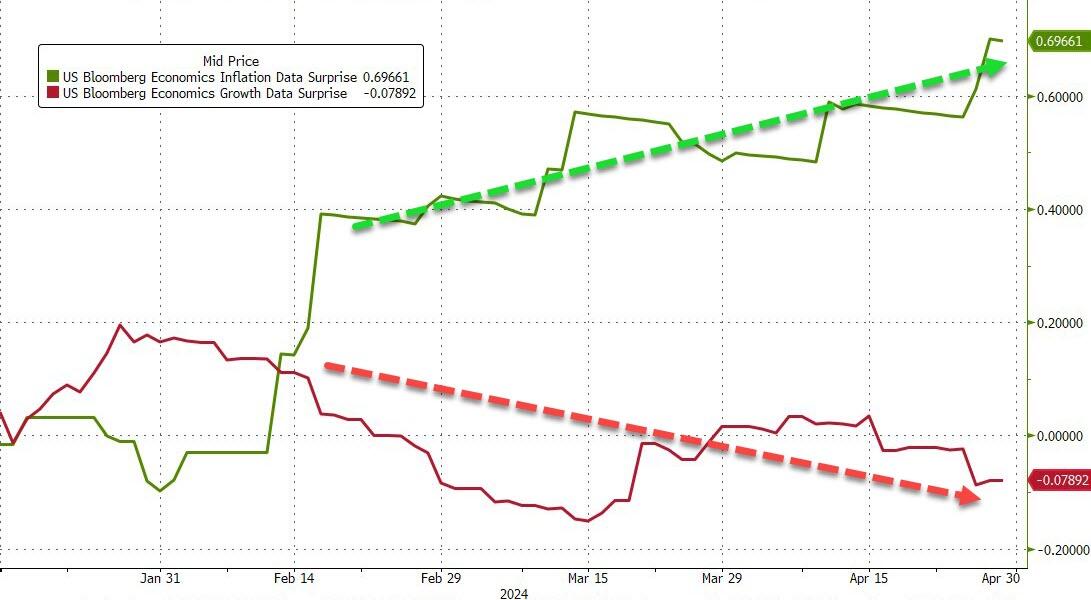

Weaker Growth And Higher Inflation… Why Consensus Was Wrong

Weaker Growth And Higher Inflation… Why Consensus Was Wrong

The weak GDP figure for the first quarter came with a double negative. Poor consumer spending and exports, plus a rise in core inflation, The US administration’s enormous fiscal stimulus, underscores the importance of considering the weaker-than-expected data.

{kind=link}

A deceleration in consumer spending, a decline in the personal savings ratio to 3.6%, and poor exports added to a set of figures for investment that were also negative when we looked at the details.

The gross domestic product is much weaker than the headlines suggest. If we look at consumption, both durable and non-durable goods were flat or down, while the only item that increased modestly was the services factor. Residential and intellectual property boosted investment, while equipment remained weak in the past two quarters. The slump in export growth coincided with a significant increase in imports, which weakened the trade deficit. Government spending continues to rise, albeit at a slower pace, and becomes the main factor to disguise what is evidently a concerning level of growth for a leading economy with enormous potential.

It is precisely because of the unnecessary increase in government spending, designed to bloat GDP and provide a false sense of strength in the economy, that inflation remains elevated and rising in a three- and six-month period.

Rising public debt has bloated the economy and left it at a disappointing level compared to its potential, as evidenced by higher inflation and weaker growth.

When the Fed’s preferred inflation measure rises to 2.8% in March from a year ago and the core PCE deflator rises to 3.1%, there is no strong economy. The propaganda repeatedly claims that the fight against inflation is over, but inflation has accelerated on a quarterly and half-year basis.

It is important to understand why these figures are negative. The average American household is poorer. Rising inflation and declining savings, non-existent real wage growth, employment-to-population, and the labor force participation rates remain below 2019 levels, and bloating GDP with an unacceptable deficit means higher taxes, lower growth, and weaker real wages in the future.

We must remember that Biden’s economic plan started with a full-blown recovery in place. This administration did not suffer the consequences of the COVID-19 lockdowns. By the time the Biden administration arrived, America was already creating almost 250,000 jobs a month.

Biden should have picked the fruits of a fast-recovering economy that is almost energy independent and therefore should not have suffered the impact of the war on Ukraine while enjoying the tail winds of the largest fiscal and monetary stimulus.

The multiplier effect of the chain of implemented government programs may have inflated GDP, but gross domestic income (GDI) presented a significantly different picture. The GDI revealed a stagnant economy with persistent inflation.

The government’s wasteful spending of newly printed money is adding gasoline to inflationary pressures, a result of careless fiscal policy and massive deficit spending. When the government prints more money than the private sector needs, inflation occurs, and the purchasing power of that money decreases.

The evidence from the past four years indicates that if the government had abandoned its spending and tax hike plans, the United States economy would have recovered better and with higher productivity growth. Despite the recovery, tax revenues fell short of expectations and spending rose to create what is now a completely unacceptable deficit.

Many economists argue that the economy is growing, and that inflation is a secondary problem. Not for the average American. Citizens are poorer in absolute and relative terms.

Consensus was wrong about the expected multiplier effect of government spending on growth and also about inflation because market participants decided to ignore monetary aggregates and the reality of unproductive spending.

Can the United States government boast this level of growth? One could argue that delivering $1.6 trillion of GDP with a $2 trillion increase in debt is not a success. This isn’t growing; it’s getting fatter. This negative situation has not improved since 2024. Every 100 days, the U.S. national debt rises by $1 trillion. Therefore, this means more taxes, less growth, and weaker real wages in the future. We can conclude that the United States’ public finances would be stronger, and the economy would be more productive if the gigantic public spending packages and tax hikes had not been implemented.

The United States administration needs to focus more on the productive sector and less on increasing the size of the bureaucratic machine. Even if the rise in mandatory spending is offset by cuts in discretionary spending, it will still be difficult to reduce debt. Therefore, prioritizing is key. Taxes are already high enough, and there is plenty of evidence that shows how the recent increase in the tax wedge for businesses and families has made the economy weaker.

The government needs to understand that it is the cause of inflation. Only the government can make all prices rise in unison and continue to increase, and it achieves this by diluting the purchasing power of the currency and issuing more than demanded.

The next two quarters are going to be key to understanding the extent of the damage caused by reckless fiscal spending.

The US government has sabotaged the Federal Reserve’s modestly hawkish policy. The public deficit has added up to $2 trillion of newly created money per year, only to deliver less economic growth and cancel out the now insignificant $1.6 trillion decline in the Fed’s balance sheet. Whether there are rate hikes or not, the Fed cannot achieve price stability if the Treasury ignores all warning signs and adds more debt.

Since 2018, the United States has added roughly $7 trillion of GDP, while the government has increased debt by $12 trillion. Implementing fiscal stimulus by increasing expenditures and raising taxes is clearly ineffective.

Markets ignore the Fed’s hawkish messages because they see insane public debt and unsustainable deficit spending, and participants know that monetary destruction will resume regardless of persistent inflation.

{kind=link}

There is plenty of time to correct the inflation and low growth problems. There is only one measure that will help: cut spending. Everything else has failed.

Tyler Durden

Mon, 04/29/2024 – 09:05

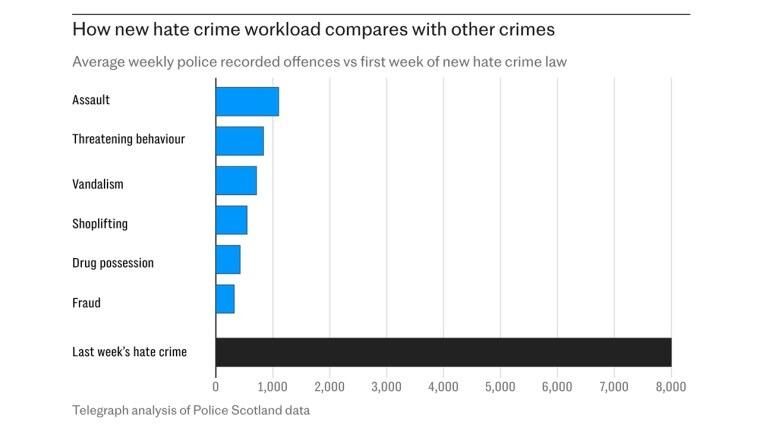

‘Anti-White’ Scottish First Minister Quits After Disastrous ‘Hate Crime Law’

‘Anti-White’ Scottish First Minister Quits After Disastrous ‘Hate Crime Law’

Scotland’s leader Humza Yousaf resigned on Monday, quitting as head of the pro-independence Scottish National Party (SNP) after scrapping a coalition agreement with Scotland’s Greens. He then failed to secure enough support to survive votes of no confidence against him expected later this week.

Yousaf, born to Pakistani immigrants in Glasgow, built an infamous reputation as a woke activist politician going into the 2023 elections. His rabid pro-immigration stance and consistent arguments in favor of DEI (Diversity, Equity and Inclusion) should have been a red flag to the Scottish public; however, with an increasingly progressive voting population Yousaf narrowly scored a victory. Here is Humza in 2020, giving a speech admonishing the “whiteness” of the Scottish government.

Scotland’s First Minister is resigning in disgrace. @HumzaYousaf’s legacy includes the hatred of Scottish people, a mainstreaming of American leftist woke politics, and a pro-Gaza foreign policy. His infamous 2020 speech before he was electedpic.twitter.com/NoPnwosEgC

— Andy Ngô 🏳️🌈 (@MrAndyNgo) April 29, 2024

Keep in mind that Scotland is 96% white. For most people logic would dictate that having a majority white government makes perfect sense given Scotland’s demographics. This is something that Yousef and his progressive ilk have set out to change.

At the beginning of 2024 the former First Minister sought to launch a pro-migrant propaganda campaign, claiming that open immigration policies lead to economic benefits for Scotland. Of course, as with all politicians that make this assertion, he offered no concrete statistics to support the theory.

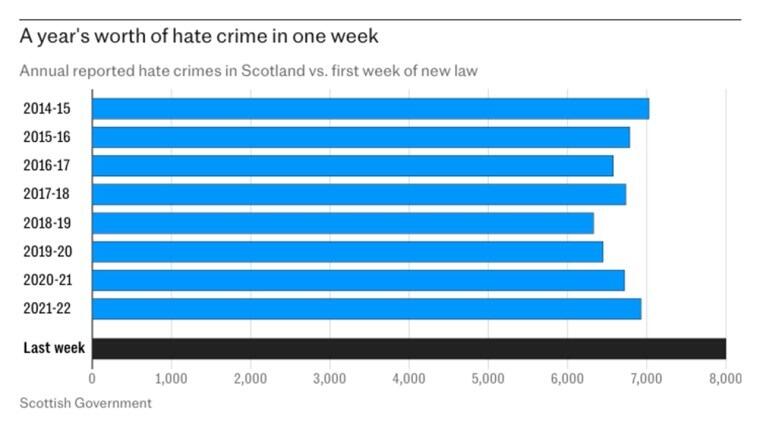

Beyond his insistence on going against the growing public opposition in Scotland to more migrants being allowed into the country, Yousaf’s biggest mistake was the passage of his now wildly unpopular “Hate Crime Act.” The law which recently went into effect criminalized many forms of speech including criticism or skepticism of gender fluid theory and trans identity. Misgendering and misuse of a trans person pronouns could now land a Scottish citizen in jail.

In response, the Scottish public flooded law enforcement agencies with fake calls accusing various trans activists and even political leaders of various hate crimes. Police were so overwhelmed by the paperwork that any effort to enforce the law has ground to a halt.

As we have detailed again and again (here, here, and here), his hate-crime law was an utter disaster – that everyone saw coming – and before his resignation, just 29 per cent of Scottish National Party voters believe Yousaf is doing a good job, while 36 per cent think he has been poor in office.

Consequently, Yousaf’s popularity among his own voters is now minus seven, down from plus 14 in January, a massive drop.

As we have highlighted, under the new ‘hate crime’ legislation, anyone deemed to have been verbally ‘abusive’, in person or online, to a transgender person, including “insulting” them could be hit with a prison sentence of up to seven years.

As a reminder, Police received 8000 ‘hate crime’ complaints in just the first week of the law coming into play, equating to more than the annual total of all hate crime reports for all previous years.

{kind=link}

The number is on course to out number the total of all other offences combined.

{kind=link}

Calum Steele, the former general secretary of the Scottish Police Federation, declared that officers “are genuinely embarrassed,” adding that “They feel that the service and by extension [they] as individual police officers will catch some of the public brunt.”

The hate crime law received backlash from every corner of the UK, including from more liberal personalities like Harry Potter author JK Rowling.

…and now, he’s gone!

{kind=link}

In an emotional address, Yousef said:

“While a route through this week’s motion of no confidence was absolutely possible, I am not willing to trade my values and principles or do deals with whomever simply for retaining power.

“Therefore, after spending the weekend reflecting on what is best for my party, for the government and for the country I lead I have concluded that repairing our relationship across the political divide can only be done with someone else at the helm.

“I have therefore informed the SNP’s national secretary of my intention to stand down as party leader and ask that she commences a leadership contest for my replacement as soon as possible.”

Scottish leader Humza Yousaf has resigned. Didn’t even make it to the election. Tip for future leaders, being racist toward 96% of your country and passing laws outlawing free speech isn’t a recipe for success. He’ll forever be known as ‘Hate Crime Humza’. pic.twitter.com/64JIXQEIQJ

— m o d e r n i t y (@ModernityNews) April 29, 2024

His decision comes two days after expressly denying that he would resign.

Humza Yousaf has resigned. Good riddance 👋🏽 pic.twitter.com/vAJjLzPAMv

— Chris Rose (@ArchRose90) April 29, 2024

Alister Jack, the Scottish Secretary, said Humza Yousaf made the right decision to resign as Scotland’s First Minister. The Tory Cabinet minister said:

“It was the right thing for the First Minister to resign.

“Humza Yousaf’s leadership has lurched from crisis to crisis from the very start, and he could not command the confidence of the Scottish Parliament.”

But, amid the political division in his coalition, as The Telegraph‘s Gordon Rayner says “Humza Yousaf’s hate crime and trans laws will be his divisive legacy“.

In truth, the public never wanted Mr. Yousaf as First Minister: opinion polls before his election consistently showed that Kate Forbes, his socially conservative rival for the leadership, was far more popular with both SNP supporters and voters as a whole.

Humza Yousaf said he will remain as First Minister of Scotland until his successor as SNP leader has been elected.

Tyler Durden

Mon, 04/29/2024 – 08:26

Futures Rise, Yen Downgraded To Banana Republic Currency After Another Rollercoaster Session

Futures Rise, Yen Downgraded To Banana Republic Currency After Another Rollercoaster Session

US equity futures swung between gains and losses and traded near session highs as US traders walked to their desks on Monday morning after a rollercoaster day for the Japanese yen, which increasingly looks like some 3rd world banana republic currency instead of belonging to the world’s 3rd largest economy, and which first plunged below 160 vs the USD – the lowest level since 1990 amid dismal volumes thanks to the Japanese market holiday on Monday – only to soar more than 500 pips in what is now the first confirmed BOJ intervention since 2022. Futures were buoyed by rising earnings optimism as traders looked ahead to another very busy week for company results, and as of 7:40am, S&P futures gained 0.2% with Nasdaq futures rising 0.3%, boosted by another surge in Tesla shares. 10Y Treasury yields fell four basis points to 4.62% ahead of today’s announcement by the Treasury of its funding needs for the coming quarter, while the dollar weakened. Oil retreated, with Brent first trading below $89 a barrel, only to rebound higher amid the endless speculation that a peace deal between Israel and Hamas is coming that would reduce geopolitical tensions in the Middle East (spoiler alert: there will be no deal). Gold rose and bitcoin fell.

{kind=link}

In premarket trading, Tesla surged 11%, slamming the recent pile up of shorts (the biggest in two years) as Elon Musk’s quick visit to China paid immediate dividends, with Tesla receiving in-principle approval from government officials to deploy its driver-assistance system in the world’s biggest auto market.

{kind=link}

Here are some other premarket movers:

Here Altimmune drops 4% after Guggenheim downgraded the stock, saying a partnership for the biotech’s lead asset pemvidutide look “increasingly unlikely.”

Apple climbs 2% after Bernstein upgraded its rating, calling issues in China “more cyclical than structural” and highlighting that the tech giant’s business in the country has tended to be more volatile than the wider company.

AT&T rises 1% as Barclays upgrades to overweight, noting the wireless carrier’s “steadier execution story.”

Paramount Global jumps 5% after Bloomberg reported that the Redstone family and Skydance Media CEO David Ellison have both offered concessions to make a possible change in control at the media company more appealing to other investors.

Shopify advances 3% after Citi raises the e-commerce company to buy, expecting solid first-quarter results following recent industry conferences and channel checks.

SoFi Technologies gains 2% after the company boosted its adjusted Ebitda guidance for the full year.

Southwest Airlines declines 1.2% after Jefferies downgraded the carrier to underperform, noting that optimization plans are languishing as delays at Boeing reduce fleets.

Tandem Diabetes rises 4% after Wells Fargo upgraded the medical device manufacturer, saying a survey indicates stable growth in insulin pumps.

The big overnight market event was the rollercoaster move in the Japanese yen which again took center stage with dramatic moves that fueled speculation over whether the government had intervened to support its beleaguered currency. In holiday-thinned trading, the yen swung wildly, rallying more than 2% on Monday after earlier dropping as much as 1.2% to 160.17 per dollar.

{kind=link}

While analysts suggested the size and speed of the jump smacked of intervention, some traders questioned that conclusion and said Japanese banks sold dollars for customers as it rallied. Japan’s top currency official, Masato Kanda, chose to keep investors guessing by declining to comment. Dow Jones reported authorities stepped in to support the yen, citing people familiar with the matter.

It is a busy week: the Fed meeting on Wednesday and US jobs report on Friday will also be critical for markets this week. The last time Fed Chair Jerome Powell spoke, he signaled that policymakers were likely to keep borrowing costs high for longer than previously anticipated, pointing to the lack of further progress on bringing inflation down, and to enduring strength in the labor market. Meanwhile, with Apple and Amazon.scheduled to report in the next few days, investors will be hoping for more evidence that big technology profits can keep propelling stocks.

Morgan Stanley’s in house permabear Michael Wilson said the pressure from higher Treasury yields is taking the shine off an upbeat earnings season; that’s even as Bloomberg data showed that 81% of S&P 500 firms have beaten first-quarter profit estimates so far. Still, as we noted over the weekend, the average stock price has barely outperformed the benchmark index on the day of results — the worst scorecard since the fourth quarter of 2020, the figures showed.

European stocks are higher, the Stoxx 600 rising 0.3% to 509.7, with Dutch medtech Philips the biggest stand-out performer, rising the most on record after striking a settlement related to a device recall; Deutsche Bank was the biggest decliner after making €1.3 billion of provisions, with its country peer Porsche falling too, following its latest earnings. Here are the biggest movers Monday:

Philips gains as much as 37%, the most on record, after the Dutch medical equipment manufacturer agreed to pay $1.1 billion to settle US claims related to the 2021 recall of sleep apnea devices

Alfen surges as much as 14% after it agreed with Dutch grid operator Liander on a new production method to avoid moisture in its Pacto transformer substations, with KBC raising the firm to buy

Anglo American shares gain as much as 4.1% after Bloomberg News reported over the weekend that BHP is considering making an improved proposal after its $39b initial offer was rejected

Unicaja Banco jumped as much as 8% to the highest level since 2018, after the Spanish lender delivered revenue ahead of expectations in the first quarter

Douglas jumps as much as 5.3% after several brokerages initiated the German perfume retailer at buy, including Citi, which called the stock a “scarce asset” in a growing category

Bravida rises as much as 6% after an internal investigation which revealed previously reported overinvoicing at the Swedish real estate services firm was very limited

Atos shares jump as much as 20%, to the highest in almost three weeks, after the IT firm got a non-binding letter of intent from the French state to acquire some parts of the business

Deutsche Bank declines 5.7%, the sharpest drop since 2023, after the German lender’s announcement that it is setting aside as much as €1.3b in legal provisions in a blow to profitability

Porsche AG shares fall as much as 4.6% after the German firm saw a “challenging” first quarter, according to analysts, who note the automaker’s headline earnings miss

Morphosys falls as much as 2.4% after a report flagged a potential issue related to experimental drug pelabresib, an issue which could complicate the planned acquisition by Novartis

Siltronic shares fall as much as 3.4% after the German wafer maker was downgraded to hold by Hauck & Aufhaeuser following a profit warning issued last week

Meanwhile, Asian equities climbed for a second straight day, as benchmarks for mainland and Hong Kong stocks looked set to enter a bull market. The MSCI Asia Pacific Index climbed as much as 0.3%, with AIA Group and TSMC among the top contributors to the gains. The MSCI China Index and Hong Kong’s Hang Seng Index were both on track to close more than 20% higher than their January lows, helped by a surge in property shares after a major Chinese developer reached a solution with bondholders for its liquidity issues.

“China may continue to outperform especially in a scenario where global risk sentiment remains cautious,” Nomura strategists including Chetan Seth wrote in a note. “Fundamentals remain tepid” and economic data in the next couple of months are important to avoid a reversal of recent gains, they added. Benchmarks in Taiwan, the Philippines and South Korea also advanced on Monday. Markets in Japan and Vietnam were closed for holidays.

In FX, the yen rallied to a 155 handle versus the dollar, having earlier weakened past 160 for the first time since 1990. The abrupt swing prompted speculation authorities may have intervened, although Japan’s top currency official has declined to comment even as Dow confirmed intervention. The Bloomberg Dollar Spot Index is down 0.3% as the greenback loses ground versus all its G-10 rivals.

In rates, treasuries climbed with US 10-year yields falling 4bps to 4.62%, with gains supported by euro-zone bond markets, particularly France’s, outperforming after Moody’s and Fitch affirmed the sovereign’s rating Friday. April inflation numbers from Germany and Spain were taken in stride. US yields richer by 2bp to 4bp across the curve with long-end-led gains flattening 2s10s, 5s30s spreads by 1.5bp and 0.5bp on the day; 10-year remains near session low around 4.625% with bunds outperforming by around 1.5bp in the sector, French 10-year by ~3bp. On Wednesday, Treasury announces quarterly refunding, expected to follow through on its January guidance of holding off on further increases

Oil prices are lower as the US pushes to broker a peace deal between Israel and Hamas. WTI falls 0.2% to trade near $83.70. Spot gold is little changed around $2,338/oz.

Monday’s US session has few calendar events. US economic data slate includes April Dallas Fed manufacturing activity at 10:30am New York time; ahead this week are consumer confidence, ADP employment change, manufacturing PMI, ISM manufacturing, factory orders and April jobs report. Fed members are in self-imposed quiet period ahead of May 1 policy announcement.

Market Snapshot

S&P 500 futures up 0.2% to 5,142.75

STOXX Europe 600 up 0.3% to 509.67

MXAP up 0.9% to 173.90

MXAPJ up 0.9% to 540.54

Nikkei up 0.8% to 37,934.76

Topix up 0.9% to 2,686.48

Hang Seng Index up 0.5% to 17,746.91

Shanghai Composite up 0.8% to 3,113.04

Sensex up 1.2% to 74,584.25

Australia S&P/ASX 200 up 0.8% to 7,637.38

Kospi up 1.2% to 2,687.44

German 10Y yield little changed at 2.55%

Euro up 0.2% to $1.0719

Brent Futures down 0.6% to $88.94/bbl

Gold spot up 0.1% to $2,339.61

US Dollar Index down 0.31% to 105.61

Top Overnight News

Tesla CEO Musk made a surprise visit to Beijing with media reports saying he aims to discuss enabling autonomous driving mode on Tesla cars in China. Later, it was reported Tesla is to partner with Baidu for China self-driving approval, according to Bloomberg. (BBC/Bloomberg) Separately, two US Senators say NHTSA should require Tesla to restrict autopilot use to certain roads.

White House said President Biden approved the Kansas disaster declaration and ordered federal assistance to supplement recovery efforts in areas affected by severe winter storm from January 8th-16th.

Apple intensified talks with OpenAI for iPhone generative AI features in which they are discussing the terms of a possible agreement and how the OpenAI features would be integrated into Apple’s iOS 18, according to Bloomberg. EU says that Apple’s (AAPL) iPad operating system has been designated as a gatekeeper under the EU DMA; apple has six months to comply with EU tech rules.

Paramount is reportedly preparing to fire CEO Bakish, via FT citing sources; additionally, sources add that the Co. is expected to receive a counterbid from Sony and Apollo this week to the offer from Skydance Media. (FT)

China’s industrial profits fell in March and slowed gains for the quarter compared to the first two months, raising doubts about the strength of a recovery for the world’s second-biggest economy. Cumulative profits of China’s industrial firms rose 4.3% to 1.5 trillion yuan ($207.0 billion) in the first quarter from a year earlier, NBS data showed, slower than a 10.2% rise in the first two months. RTRS

China’s banking regulator warns the country’s regional banks to stop piling into long-term government bonds as they could be hit with heavy losses if rates rise. FT

Japan’s currency surged as much as 5 yen against the dollar on Monday, with traders citing heavy dollar-selling intervention by Japanese banks for the first time in 18 months after the yen hit fresh 34-year lows earlier in the day. RTRS

Russia is expected to launch a new large-scale offensive in May or June (although the influx of American weapons will make Ukraine better positioned to withstand the onslaught). FT

Ukraine isn’t expected to regain offensive momentum until 2025 at the earliest and has no clear military path to recapturing the ~20% of the country stolen by Russia. WaPo

BHP is considering an improved bid for Anglo American, people familiar said. The miner may need to find over $9 billion in cost savings from the tie-up to raise the offer, which may be a stretch. BBG

Apple’s iPad was hit by the EU rules aimed at stopping potential competition abuses before they take hold. Apple now has six months to make sure its tablet ecosystem complies with preemptive measures. BBG

AAPL has renewed negotiations w/OpenAI and remains in talks w/Google about incorporating AI-linked technology into the next version of iOS (investors expect to hear a lot more about Apple’s plans at the upcoming WWDC). BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the week on the front foot after the tech-led surge last Friday on Wall St and amid increased optimism regarding a Gaza truce with negotiators set for talks in Cairo on Monday, although Japan was on holiday and ahead of this week’s key risk events. ASX 200 was led higher by real estate, tech and telecoms owing to softer yields. Hang Seng and Shanghai Comp. gained with the former entering into bull market territory after climbing over 20% from its January lows, while participants digested a slew of earnings and the mainland also shrugged off the slowdown in March Industrial Profits.

Top Asian News

China’s MOFCOM said export control measures proposed by Japan on semiconductors will seriously affect the normal trade between Chinese and Japanese enterprises, as well as undermine the stability of the global supply chain. Furthermore, it stated that China urges the Japanese side to rectify its ‘erroneous practices’ in a timely manner and China will take necessary measures to firmly safeguard the legitimate rights and interests of Chinese enterprises, according to Reuters.

US and Taiwan are to hold in-person negotiation talks on trade beginning on April 29th, according to Reuters.

Japanese PM Kishida said they will promote union policies for wage increases, according to Reuters.

PBoC has reportedly expanded a warning on bond investments to regional banks, via Bloomberg citing sources.

Agricultural Bank of China (1288 HK) Q1 (CNY): Net Income 70.839bln (exp. 73.578bln), NII 144.535bln (exp. 137.021bln).

PetroChina (857 HK) Q1 (CNY): Revenue 812.184bln (exp. 833.77bln), Net +5% Y/Y, EPS 0.25 (exp. 0.24).

Japanese Top Currency Diplomat Kanda offers no comments on whether there was FX intervention; will continue to take appropriate action against excessive FX moves; does not have a specific FX level in mind. Speculative, rapid, abnormal FX moves have bad impact on the economy, so unacceptable. Ready to respond 24 hours, 365 days, when asked whether Japan was ready to take action in FX. Will disclose at the end of May if there way intervention.

European bourses, Stoxx600 (+0.3%) are almost entirely in the green, taking the lead from a positive APAC session overnight. Trade has been rangebound since the open, though has just been coming off best levels in recent trade. Basic Resources is found towards the top of the pile, benefiting from modestly firmer base metal prices and after further takeover reports regarding BHP/Anglo American. Retail marginally underperforms. US Equity Futures (ES +0.2%, NQ +0.3%, RTY +0.3%) are entirely in the green, posting modest gains in tandem with European peers. In terms of pre-market movers; Apple (+1.5%) gains on reports that it has resumed talks with OpenAI. And Tesla (+6.5%) benefits from news that the Co. has received tentative approval for its self-driving service.

Top European News

ECB’s Wunsch (interview from 20th April) said ECB should be cautious regarding a July cut, should be cautious regarding a larger-than-25bps cut in June. Base case it as least two cuts, “but if we only do two or even three cuts, then we shouldn’t communicate that we’re going to cut at every meeting”. Don’t think ECB has sufficient data to have confidence on 100bps of cuts throughout the year. On what could get in the way of a June cut, Wunsch said “really bad news”, “two bad readings on the inflation front or other major developments.”

Spanish PM says he has decided to stay on as Prime Minister.

Scotland’s First Minister Humza Yousaf is set to step down after coming to the conclusion that is position is no longer tenable, according to The Sunday Times.

Fitch affirmed France at AA-; Outlook Stable and affirmed Switzerland at AAA; Outlook Stable, while it affirmed Sweden at AAA; Outlook Stable.

FX

USD is softer vs. peers in the wake of aggressive USD/JPY selling overnight and into the European morning. From a technical perspective, DXY has been as low as 105.46 but is respecting Friday’s 105.41 base.

JPY was volatile overnight and initially surged above 160.00 with no obvious catalysts and with Japanese participants away from the market. The pair later saw a sharper drop and breached 156.00 to the downside in the absence of any obvious drivers; some have speculated potential intervention. Since, USD/JPY has continued to bleed, going as low as 154.54 (currently 155.80).

EUR is firmer vs. USD (as is the case for all major peers). Focus in the Eurozone today is on the German national CPI at 13:00BST, with regional releases thus far broadly showing increases on a M/M and Y/Y basis, though initial reaction dovish as the core numbers continue to moderate. 1.0733 is the high thus far and yet to approach Friday’s best of 1.0753.

Antipodeans are benefitting from the broadly softer USD. AUD/USD is now up for a 6th consecutive session with focus on a test of 0.66 after printing a session high of 0.6586.

Japan’s Top currency diplomat Kanda said will not comment now, when asked about whether Japan intervened in the currency market.

PBoC set USD/CNY mid-point at 7.1066 vs exp. 7.2759 (prev. 7.1056).

Fixed Income

USTs are bid with specifics light so far and direction drawn from EGB action after the regions core inflation numbers from Spain & German. Currently at the top-end of a 107-18+ to 107-27+ range with the 10yr yield below 4.65% but in familiar ranges.

Bunds are firmer with markets focussing on the continued moderation in core Spanish and German state CPI into the 13:00BST nationwide German number. Bunds peaked at 130.87 having pared knee-jerk pressure of around 20 ticks on the German headline numbers; now off best levels.

Gilts are a touch firmer but yet to move significantly from the unchanged mark in a narrow circa-20 tick range with specifics light and direction for today and this week broadly likely to come from European and US events. Currently at 96.25 shy of Friday’s 96.33 best and then 96.67 from Wednesday thereafter.

Italy sells EUR 6.75bln vs exp. EUR 5.75-6.75bln 3.35% 2029, 3.85% 2034 BTP and EUR 3.5bln vs exp. EUR 3-3.5bln CCTeu.

EU sells EUR vs exp. EUR 2.5bln 3.125% 2028 and EUR 2.5bln 2.75% 2033 EU Bond.

Commodities

A subdued day for the crude complex despite the weaker Dollar, but amid the lack of geopolitical escalation over the weekend and amid more sanguine atmosphere surrounding the latest Israel-Gaza ceasefire talks. Brent counterpart slipped from USD 89.25/bbl to USD 88.43/bbl.

Mixed trade across precious metals with only spot silver benefiting from the slide in the Dollar, whilst spot gold sees its upside capped by the lack of geopolitical escalation and ahead of FOMC later this week. XAU clambered off its USD 2,319.84/oz intraday low but is yet to reach highs seen on Friday at USD 2,352.64/oz.

Base metals are mixed with some of the market benefiting from the softer Dollar, albeit modestly; 3M LME copper trades on either side of USD 10,000/t.

TotalEnergies (TTE FP) CEO said the Co. is expected to complete the first phase of the solar power project in Iraq within the next year, while the Co. is to complete the first stage of utilising the by-produced gas from Iraq’s project during 2025 with a production capacity of 50mln cubic feet, according to Reuters.

Turkey is in talks with ExxonMobil (XOM) over a multi-billion dollar LNG deal, according to FT.

Geopolitics: Middle East

“Al-Arabiya sources: An Israeli delegation will head to Cairo tomorrow and the plan is indirect negotiations with Hamas”

UKMTO said it has receives a report of an incident 54NM Northwest of Yemen’s Mokha

Egypt offered a new proposal for a truce between Israel and Hamas in which some Israeli hostages would be exchanged for Palestinian prisoners and a three-week ceasefire, while Egyptian officials said Israel helped create the proposal and would enter longer-term discussions once Hamas releases the first group of 20 hostages over the truce period, according to WSJ.

Hamas said it received Israel’s official response to its position over ceasefire talks and will study the proposal before submitting its response. It was later reported that a Hamas official told AFP that there were no major issues in the group’s remarks on the truce proposal, while it was separately reported that a Hamas delegation is to visit Cairo on Monday for ceasefire talks, according to an official cited by Reuters.

Israel’s Foreign Minister said Israel will suspend the planned operation in Rafah if Hamas agrees to a hostage deal and stated the release of hostages is their top priority. It was also reported that the Israeli military said the amount of aid going into Gaza will scale up in the coming days.

Palestinian President Abbas said Israel will go into Rafah in the next few days and the US is the only country that can stop Israel from attacking Rafah, while he is worried that Israel will try to push Palestinians out of the West Bank after it is done with Gaza, according to Reuters.

Medical official said at least 13 Palestinians were killed in Israeli airstrikes on three houses in Rafah in southern Gaza, according to Reuters.

US President Biden spoke with Israeli PM Netanyahu on Sunday and reaffirmed his ironclad commitment to Israel’s security, as well as stressed the need for progress in aid deliveries to be sustained and enhanced in full coordination with humanitarian organisations. Furthermore, they discussed Rafah and Biden reiterated his clear position, according to the White House cited by Reuters.

White House national security spokesperson Kirby said Israel assured the US that they won’t go into Rafah until the US has a chance to share its perspectives and concerns, while he added Israelis have started to meet the aid commitments that US President Biden asked them to meet. It was separately reported that US Secretary of State Blinken will travel to Jordan and Israel following Saudi Arabia, according to Reuters.

France’s Foreign Minister said to make proposals in Lebanon to stabilise the zone and prevent a war between Hezbollah and Israel, according to Reuters.

UKMTO said it received reports of an incident 177 nautical miles southeast of the Port of Nashtoon located in eastern Yemen on Saturday night which involved a small boat that approached a ship, although there was no harm or damage and the ship carried on its journey, according to IRNA.

OTHER

US intelligence found that Russian President Putin did not directly order Navalny’s death in February, according to WSJ. US intelligence report does not dispute Putin’s culpability for the death of Navalny but believes he probably did not order it at that moment, while a Kremlin spokesperson called the intelligence report empty speculation.

Russian Foreign Ministry said there will be a severe response if Russian assets are touched and it is a pity that some in the West do not understand it, while it was also reported that Russia’s Kremlin said there will be endless legal challenges if Russian assets are seized.

Russia’s Kremlin said there are no grounds to hold any peace talks with Ukraine given Kyiv’s official refusal to conduct such talks with Russia.

Kyiv’s top general said fighting on the eastern front worsened and Ukrainian troops had fallen back in three places.

North Korea’s Foreign Ministry said it will make stern and decisive choices in response to the US using human rights for anti-North Korean behaviour, while it added that the US envoy on North Korean human rights is motivated politically and is considered political provocation, according to KCNA.

US Event Calendar

10:30: April Dallas Fed Manf. Activity, est. -11.3, prior -14.4

DB’s Jim Reid concludes the overnight wrap

I wrote some of this while supervising my three kids doing their homework this weekend. The 6yr old twins had fractions and adverbs, with the latter being pretty challenging. They had a whole story where they had to insert missing adverbs. It was incredibly, astonishingly, extremely, exceedingly, enormously, supremely, difficult. So if you see a few stray adverbs below it’s because I’ve been swimming in them this weekend.

With just two days left of a difficult April for markets, last week actually saw the best week for the S&P 500 (+2.67%) and NASDAQ (+4.23%) since November as earnings generally gave markets a boost even if the US inflation data was net net worrying. You’ll see our full recap of last week towards at the end but looking forward first it’s an exceptionally busy week of important events.

The FOMC conclusion on Wednesday is the obvious highlight (full preview below) but we also have payrolls on Friday to look forward to. DB expect a more hawkish-leaning Fed this week. While our economists expect the Committee will maintain an easing bias (preview here), they do expect the statement and press conference to echo Chair Powell’s view that firmer inflation prints suggest it will take longer to gain confidence about disinflation. The press conference will be fascinating to see the nuances in Powell’s responses as he justifies a likely unchanged easing bias, even if the rhetoric is more hawkish, in the face of rising inflation.

In terms of the jobs report on Friday, our US economists see payrolls gaining +240k in April (consensus +250k), down from +303k in March. The consensus expects the unemployment rate and the hourly earnings growth rate to stay at 3.8% and +0.3% MoM, respectively, although DB expects the former to tick up a tenth. Overall the market sees a solid report.

Other key data in the US includes consumer confidence tomorrow, the manufacturing ISM, JOLTS, and ADP on Wednesday, and the services ISM on Friday. We also see the latest US Treasury quarterly refunding announcement on Wednesday, after the borrowing estimate is due today. This was a big pivot point for global markets back in August (negative) and October (positive) but since then a commitment not to increase auction sizes has reduced its importance. Our strategists preview the event and detail their estimates here. Finally in the US, earnings season maintains its peak pace as 174 report in the S&P versus 180 last week with Amazon (Tuesday) and Apple (Thursday) the obvious highlights. Meanwhile, 66 Stoxx 600 companies will report this week.

In Europe, preliminary CPI reports for Germany and Spain today, and the Eurozone tomorrow will have a lot of significance for the June ECB meeting and whether we will see the first cut. Our European economists preview the release here. For the Eurozone, they expect the headline HICP to fall one-tenth to 2.31% yoy, its lowest value since August 2021 and see core inflation slowing further to 2.45% yoy, 0.50pp lower than in March 2024. Staying in Europe the latest GDP data for Germany, France, Italy and the Eurozone are due tomorrow. In Asia, various China PMIs (tomorrow) will be a big focus and in Japan, several key economic indicators are also due, including industrial production and labour market data tomorrow.

The day-by-day calendar at the end as usual gives a more detailed diary of the main events this coming week.

Asian equity markets have started the week on a positive note extending Friday’s rally on Wall Street. Chinese stocks are the best performers across the region with the Hang Seng (+1.93%) leading gains followed by the CSI (+1.63%) and the Shanghai Composite (+0.94%), buoyed by a rally in property stocks after embattled property developer CIFI Holdings reached a solution with bondholders on a plan to restructure its offshore debt. Elsewhere, the KOSPI (+0.91%) is also trading higher while stock markets in Japan are closed for a public holiday, also meaning no cash Treasury trading as yet. S&P 500 (+0.25%) and NASDAQ 100 (+0.34%) futures are edging higher.

In FX, the Japanese yen remained under pressure as it weakened past 160 earlier (from just below 158 at the open), its weakest level since 1990. This was in thin holiday trading and it’s subsequently bounced back to below 156. So some astonishing moves this morning!

Over the weekend, China’s industrial profits fell -3.5% in March (YoY) and have now risen + 4.3% y/y in the first quarter, significantly down from a +10.2% expansion in the January-February period, thus still pointing to challenges for China even with a better outlook of late.

Recapping last week now, the US March PCE inflation came in line with expectations on Friday at +0.3% month-on-month, allowing markets to breathe a slight sigh of relief compared to the strong Q1 PCE deflator in the GDP data the day before. In year-on-year terms, the March PCE release came in just above expectations at +2.7% (vs 2.6% expected). The month-on-month core print was also in line with consensus at +0.3%, and at +2.8% year-on-year (vs 2.7% expected). The March data also pointed to a still vibrant US consumer, with real personal spending up +0.5% on the month (vs +0.3% expected).

With the PCE print largely in line with expectations, US equities rallied, with the S&P 500 rising +1.02% on Friday. A strong performance by the tech giants following strong Q1 results from Alphabet (+10.22%) and Microsoft (+1.82%) the previous evening saw the Magnificent Seven post their best day in two months (+3.27%). After three weeks of consecutive losses, both the S&P 500 (+2.67%) and the NASDAQ (+4.23%) saw their largest weekly gains since last November. Even as technology spearheaded the rally, the gains were broad-based, as the Russell 2000 index rose +2.79% (and +1.05% on Friday). European equities also advanced, with the STOXX 600 up +1.74% last week (and +1.11% on Friday). The FTSE 100 hit another record high after gaining +3.09% (and +0.75% on Friday).

Friday’s PCE print did little to reverse expectations for fewer Fed rate cuts this year. The number of cuts anticipated by the December meeting was unchanged on Friday (+0.1bps) but down -4.9bps over the week to 34bps, with the decline coming on Thursday following the inflation data within the Q1 GDP release. US Treasuries did see a moderate rally on Friday, as the 2yr and 10yr yields fell -0.3bps and -4.0bps respectively. However, this was insufficient to erase earlier losses with Treasury yields seeing their highest weekly close year-to-date, up +0.9bps to 4.996% for 2yrs and +4.3bps to 4.665% for 10yrs. The story was similar in Europe, as investors dialled back their expectations of ECB rate cuts by -2.2bps on the week to 72bps. This saw 10yr bund yields rise +7.5bps on the week to 2.57%, despite a sizeable recovery on Friday (-5.5bps).

Meanwhile in Asia, the major story last week was the weakening of the Japanese yen. With the Bank of Japan leaving interest rates on hold, alongside restrained commentary on the exchange rate by policymakers, the yen fell -2.33% (and -1.78% on Friday) to 158.33 per dollar, its weakest level since 1990. Against this backdrop, the Nikkei 225 rose +2.34% (and +0.81% on Friday).

Finally in commodities, copper secured its fifth consecutive week of gains after rising +1.48% (and +1.03% on Friday) on the back of growing demand for clean transition metals and tight supply. On the other hand, gold ended its five-week streak of consecutive gains, falling -2.26% (+0.39% on Friday) amid easing geopolitical fears.

Tyler Durden

Mon, 04/29/2024 – 08:23

Tesla Jumps After China Greenlights Full-Self Driving With Baidu

Tesla Jumps After China Greenlights Full-Self Driving With Baidu

Tesla shares jumped in premarket trading in New York after Bloomberg reported that Beijing had given Tesla the ‘greenlight’ to roll out its driver-assistance system, known as “Full Self-Driving,” or FSD, in the world’s largest car market.

Sources say Tesla will partner with Chinese tech giant Baidu for mapping and navigation software to support FSD. Tesla also has multiple data security and privacy requirements that satisfy the country’s regulators.

In a separate report, The Wall Street Journal said, “Beijing has tentatively approved the company’s plan to launch FSD.”

The approval comes one day after Elon Musk unexpectedly visited Beijing on Sunday and met with Premier Li Qiang, who was previously the Communist Party chief in Shanghai when Tesla was setting up its automobile manufacturing plant there.

WSJ said Musk also met with Robin Zeng, chairman of Tesla battery supplier Contemporary Amperex Technology, in Beijing.

Wedbush Securities senior analyst Dan Ives told Bloomberg TV that Musk’s weekend visit to China was a major “watershed moment.”

“This could open up FSD in China, which I view as unlocking what really could be the golden opportunity for them,” Ives said.

FSD approval in China would be a massive win for Tesla, given the company’s year-over-year decline in quarterly revenue since 2020. The worsening EV price war with other EV makers and legacy automakers, in addition to high interest rates curbing demand, has forced the company to reduce its global headcount by 10%.

News of China’s backing of FSD sent Tesla shares up 8% in premarket trading in New York.

{kind=link}

As of Friday’s close, shares are down 32% this year, while 3.84% of the float is short, equivalent to about 106 million shares. Short interest has hit a three year high.

{kind=link}

On an earnings call last week, Musk said, “We plan on, with the approval of the regulators, releasing it as a supervised autonomy system in any market that — where we can get regulatory approval for that, which we think includes China.”

Tyler Durden

Mon, 04/29/2024 – 07:45

When Life Imitates Apocalypse Culture…

When Life Imitates Apocalypse Culture…

Authored by Mark Jeftovic via BombThrower.com,

Real world “cancer cure” eerily mirrors zombie flick setup

If anybody remembers the opening segment from the Will Smith zombie apocalypse flick I Am Legend, it starts with a comically ironic scene wherein a precocious female scientist, endearingly played by Emma Thompson proudly announces a “cure for cancer” that involves reprogramming the measles virus to act more beneficially toward its human host – thereby eradicating cancer cells, and thus, the disease itself:

The scene cuts… to the apocalyptic fall of New York City, which we learn is occurring globally because that cancer cure didn’t actually cure cancer – it instead turned into a contagious virus (stop me if you’ve heard this one before), and wiped out 90% of the population. Then it turned most of the survivors into zombies.

The movie is itself a reboot of the 1971 film “Omega Man” starring Charleston Heston, and both are based on the 1954 Richard Matheson novel titled “I Am Legend”.

When I saw a tweet from the Right Said Fred guys this morning, I could not get over how uncannily this real world clip of a female scientist extolling the benefits of an MRNA vaccine that cured cancer in mice rhymed with the Hollywood dramatization years earlier:

Once again I’ll pass, but thanks for the heads up. https://t.co/KTGClnOKnM

— Right Said Fred (@TheFreds) April 28, 2024

Here we have British writer and GP, Dr. Renee Hoenderkamp, who could easily be cast as Emma Thompson in any ensuing biopic, describing a process of taking the “technology learned from Covid” and repurposing it to kill cancel cells within the human body.

So far they’ve been testing it on mice with a 50% success rate.

Interviewer: So, is this as big as it sounds?

Hoenderkamp: I think it potentially is. I mean, it’s very early days. So basically they’ve discovered that if they use the same technology that they use for COVID, and they use some mRNA, which is a messenger part of DNA, they take your particular cancer, they biopsy it, they take some of the protein on your cancer, and they put it back into your cells, and they tell your cells to make that protein.

The idea is that your body then makes antibodies against it. It gets the memory cells, the t cells, the ones we heard about, lots in COVID. And so then after you’ve been treated for your cancer, if any of those cells are still floating around, or if any of them start to come back and multiply, your own immune system will recognize them from that vaccine and kill it.

We all know what happened next in “I Am Legend”:

Basically, this 👇https://t.co/vWK4U67Poq

— Mark Jeftovic, The ₿itcoin Capitalist (@StuntPope) April 28, 2024

It’s odd how life seems to be imitating art, specifically, zombie apocalypse flicks (but only for anti-vaxxer nut-jobs, apparently).

{kind=link}

(Also worth noting that the Bill Gates, and sundry globalists plan to spray aerosols into the atmosphere to slow global warming is the exact setup and premise of “Highlander II: The Quickening“, the sequel to the earlier movie albeit a box office flop).

We know from two years of Covid malfeasance (not to mention other mass scale bunglings) that whatever our technocratic overlords dream up in order to usher in utopia, the unintended consequences will dwarf their ability to cope and push us all further into The Jackpot (defined as a period of rolling catastrophes and never-ending crises that began in earnest with the 2019 lab leak that ignited the pandemic).

* * *

My next e-book The CBDC Survival Guide: Navigating Monetary Apartheid will be out soon (honest), sign up for The Bombthrower mailing list and I’ll let you know when it drops – and get a copy of the The Crypto Capitalist Manifesto in the meantime.

Follow me on Twitter or Nostr. npub1elwpzsul8d9k4tgxqdjuzxp0wa94ysr4zu9xeudrcxe2h3sazqkq5mehan

Tyler Durden

Mon, 04/29/2024 – 07:20

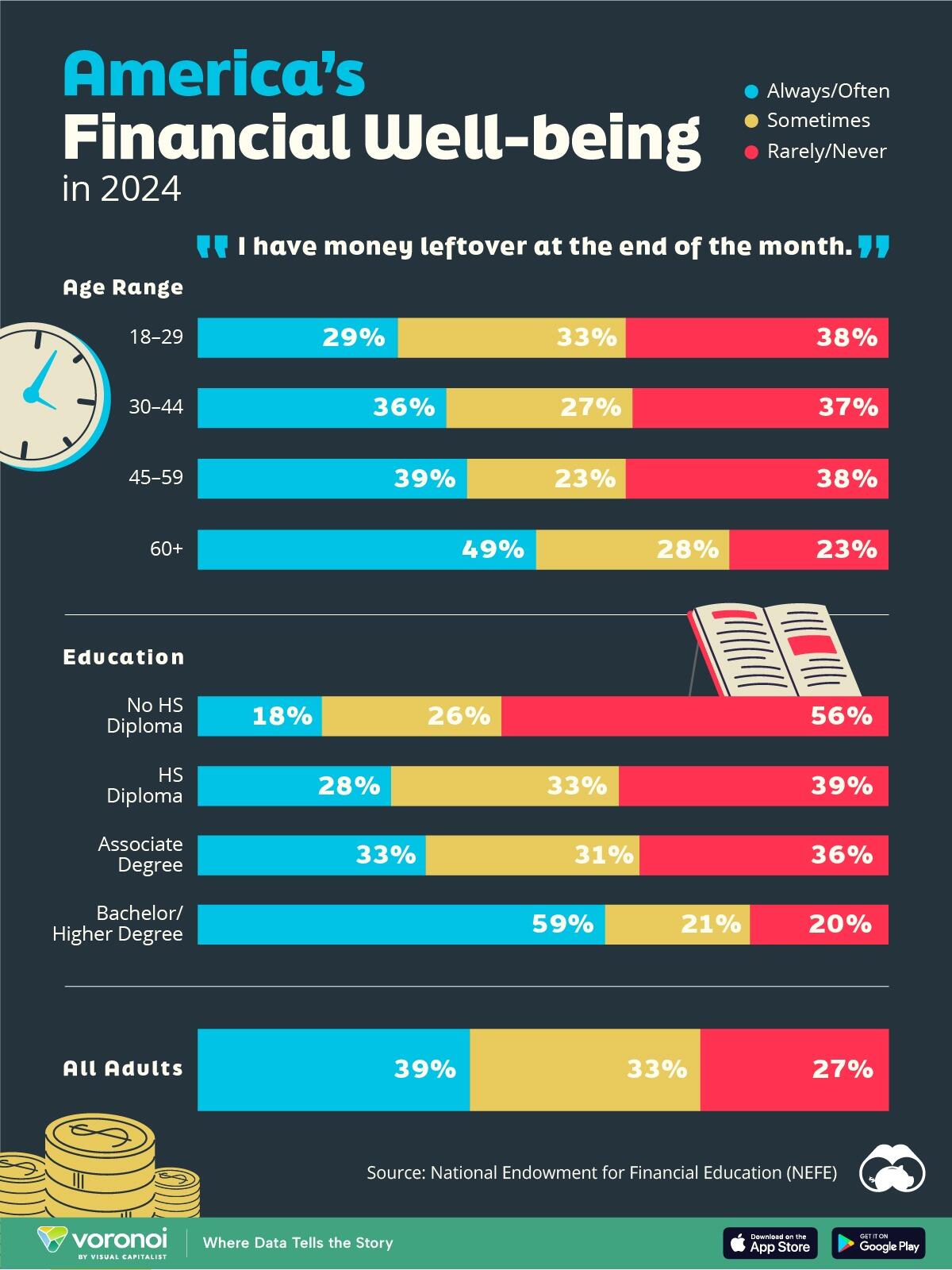

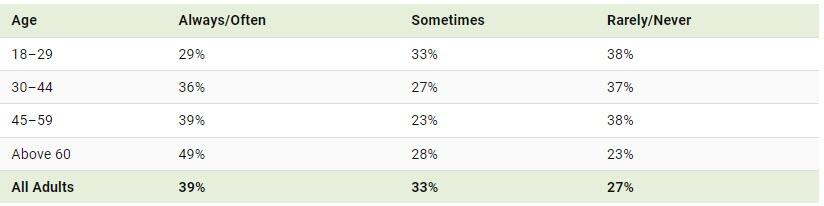

Who Has Savings In This Economy?

Who Has Savings In This Economy?

Two full years of inflation have taken their toll on American households. In 2023, the country’s collective credit card debt crossed $1 trillion for the first time. So who is managing to save money in the current economic environment?

Visual Capitalist’s Pallavi Rao visualizes the percentage of respondents to the statement “I have money leftover at the end of the month” categorized by age and education qualifications. Data is sourced from a National Endowment for Financial Education (NEFE) report, published last month.

The survey for NEFE was conducted from January 12-14, 2024, by the National Opinion Research Center at the University of Chicago. It involved 1,222 adults aged 18+ and aimed to be representative of the U.S. population.

{kind=link}

Older Americans Save More Than Their Younger Counterparts

General trends from this dataset indicate that as respondents get older, a higher percentage of them are able to save.

{kind=link}

Note: Percentages are rounded and may not sum to 100.

Perhaps not surprisingly, those aged 60+ are the age group with the highest percentage saying they have leftover money at the end of the month. This age group spent the most time making peak earnings in their careers, are more likely to have investments, and are more likely to have paid off major expenses like a mortgage or raising a family.

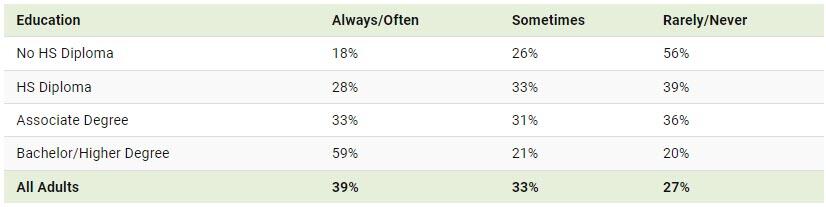

The Impact of Higher Education on Earnings and Savings

Based on this survey, higher education dramatically improves one’s ability to save. Shown in the table below, those with a bachelor’s degree or higher are three times more likely to have leftover money than those without a high school diploma.

{kind=link}

Note: Percentages are rounded and may not sum to 100.

As the Bureau of Labor Statistics notes, earnings improve with every level of education completed.

For example, those with a high school diploma made 25% more than those without in 2022. And as the qualifications increase, the effects keep stacking.

Meanwhile, a Federal Reserve study also found that those with more education tended to make financial decisions that contributed to building wealth, of which the first step is to save.

Tyler Durden

Mon, 04/29/2024 – 06:55

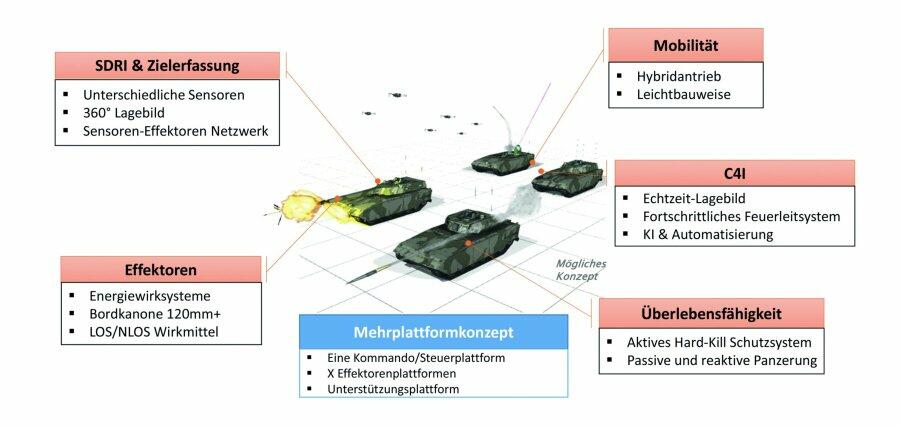

EU Begins ‘Tank Of Future’ Development After Russia Annihilates Leopard 2 Tanks In Ukraine

EU Begins ‘Tank Of Future’ Development After Russia Annihilates Leopard 2 Tanks In Ukraine

German Defense Minister Boris Pistorius and his French counterpart, Sebastien Lecornu, announced Friday the two countries will produce the next-generation battle tank to replace Germany’s Leopard 2 tank that will land on modern battlefields in the late 2030s or early 2040s.

“It’s not about making a Leopard 3 or 4; it’s about designing something brand new,” German defense minister Pistorius said, as quoted by Euronews.

{kind=link}

Pistorius said the next-gen main battle tanks will be equipped with artificial intelligence and will not require “human pilots.”

French defense ministry Lecornu said KNDS, Rheinmetall, Thales, and other defense manufacturers will begin work on the ‘tank of the future’—formally known as the Main Ground Combat System (MGCS).

Developing a next-generation tank comes as there have been countless reports that Russian armed forces have destroyed Leopard 2 tanks operated by the Ukranian Army.

Confirmed: Russians Just Destroyed Their First Leopard 2 Tank, Bradley Fighting Vehicles

And this…

Ukraine’s Leopard 2 Tanks Are Nearly All Destroyed Or Broken

Germany and France are also pushing to build the next-generation fighter jet, called the Future Combat Air System, which is set to enter service in 2040, along with integrated drone fleets.

The trend is that a world emerging into a multi-polar state has sparked a surge in military spending worldwide.

A new Stockholm International Peace Research Institute report detailed how global military expenditures hit a record high of $2.44 trillion in 2023.

We’ve diligently noted that the defense sector is in a bull market:

World Stumbles Into “More Dangerous Decade” As Defense Spending Soars, Says Military Think Tank

Germany Reportedly Goes On Military Spending Spree To Hit NATO Spending Minimums For First Time

Lockheed Martin Wins $17BN Interceptor Contract To Protect US Homeland

German Tank Builder Says “New Decade Of Security Policy Begins” As Defense Bull Market Roars

SAAB CEO Says Rising War Risk Drives Defense Spending; Missile Stocks In Bull Market

Global defense stocks, tacked by MSCI, have surged to record highs.

{kind=link}

The chaos in the world is not going away. Everything is up for grabs.

Tyler Durden

Mon, 04/29/2024 – 05:45